Robotics in 2026 is booming, with advancements shaping industries like manufacturing, healthcare, and logistics. The sector raised €37.9 billion in 2025, and leaders like NVIDIA, Amazon, and Tesla are driving progress in industrial robots, humanoids, and AI infrastructure. Here’s a quick breakdown:

- Industrial Robots: Amazon's "Sequoia" system increased warehouse efficiency by 75%, while Tesla's Optimus humanoids are scaling up to 50,000 units by year-end.

- Healthcare: Robotic surgeries account for 60% of procedures in major hospitals, with systems like Intuitive Surgical's da Vinci 5 leading the market.

- Humanoids: Tesla and China's AgiBot dominate, but battery life and reliability challenges remain.

- Logistics: Amazon's 1 million-robot fleet now handles 75% of global deliveries.

- AI Infrastructure: NVIDIA's GR00T and Jetson platforms power robotics innovation.

Despite progress, challenges like short robot battery life (90–120 minutes) and performance drops outside labs (from 95% to 60%) persist. The industry's future depends on addressing these limitations while scaling production and diversifying supply chains.

1. Industrial Robotics

Technology Maturity

Industrial robotics has come a long way, moving from rigidly scripted routines to Physical AI - systems capable of perceiving and adapting in real time instead of just following pre-set rules [4,8]. While tasks like warehouse navigation and simple item picking have reached a commercial level, more intricate operations like multi-step assembly remain in testing phases [5]. For instance, a robotic policy that can achieve 95% accuracy in controlled lab environments often drops to around 60% reliability when faced with real-world challenges like varying lighting conditions or material textures [1].

Companies like NVIDIA are making bold moves in this space, aiming to become the "Android of robotics" with their Isaac and GR00T platforms. These tools connect over 2 million developers to a shared framework, while players such as Physical Intelligence and Ant Group are working on Vision-Language-Action (VLA) models. These VLA systems allow robots to interpret natural language commands and translate them into immediate physical actions [1,8]. This shift toward using foundation models - pre-trained on massive datasets - is proving more effective than building task-specific models from scratch [5]. Such advancements are shaping how the industry evolves.

Market Impact

By early 2026, the global market for industrial robot installations reached an estimated €15.8 billion [6]. In June of the same year, Amazon revealed its "Sequoia" system, which improved inventory identification and storage speeds by 75% compared to older methods. Additionally, their "DeepFleet" AI model enhanced robot travel efficiency by 10% across fulfilment centres [1,4].

Real-world trials are also illustrating the potential and limitations of robotics. Over 11 months at BMW's Spartanburg plant, Figure AI's Figure 02 robot successfully loaded more than 90,000 parts into 30,000 BMW X3 vehicles during 10-hour shifts. Despite its technical success, the robot operated at only a quarter of the speed of human workers, leading to a redesign of its hardware [1,6].

Innovation Approach

A growing trend in the industry is the adoption of Agentic AI, which blends analytical AI for structured decision-making with generative AI to improve adaptability [6]. The convergence of IT and OT (information and operational technologies) is also enabling real-time data sharing between digital twins and physical hardware [6]. For example, specialised processors like the NVIDIA Jetson T4000 (€1,899 per unit) are now handling high-frequency manipulations directly onsite, reducing the need for cloud-based processing [1].

"The conversation is shifting from what robots could do to what they can reliably do in the real world."

– Steve Crowe, Executive Editor, The Robot Report [10]

Several cutting-edge deployments highlight this hybrid innovation. CATL, for instance, has introduced humanoid robots in its battery manufacturing lines. These robots achieve 99% reliability when inserting connectors into battery packs and can match human speeds, even when working with challenging, flexible cables [5]. Investment in "world models" - AI systems designed to predict environmental changes - has also seen a dramatic rise, growing from €1.3 billion in 2024 to €6.5 billion in 2025 [7].

sbb-itb-e314c3b

2. Medical and Surgical Robotics

Technology Maturity

Medical and surgical robotics have come a long way, evolving from basic mechanical tools to systems capable of adapting in real time [3]. Intuitive Surgical leads the pack with its da Vinci 5 platform, which boasts computing power that’s 10,000 times greater than its earlier models. This technological leap allows for real-time risk assessment and even automated suturing [13]. With more than 10,000 da Vinci units deployed globally, the system has been used in over 12 million procedures [11].

In December 2025, the field saw a major development when Medtronic's Hugo RAS and CMR Surgical's Versius Plus received FDA clearance [15]. These systems bring a fresh approach with modular, mobile-cart designs that improve flexibility in operating rooms. Another standout is Asensus Surgical’s Senhance system, which introduces haptic feedback - a feature that lets surgeons sense tissue resistance during procedures, a capability absent in earlier platforms [11].

These advancements are already redefining how surgeries are performed and reshaping the competitive landscape in the market.

Market Impact

The robotic surgery market is undergoing a transformation. By 2026, the global market for robotic surgical procedures hit €14.3 billion and is projected to grow to an impressive €49.1 billion by 2034, with a compound annual growth rate of 16.68% [12]. North America dominates the market with a 73.89% share, and 60% of large hospitals worldwide have adopted robotic surgical systems [1]. The benefits of AI-assisted robotic surgery are clear: it reduces operative time by about 25%, lowers intraoperative complications by 30%, enhances surgical precision by 40%, and shortens patient recovery by 15% [17].

One remarkable example of this technology in action took place in May 2025. A team at Shanghai Ninth People's Hospital, led by Director Yixin Zhang, used KouTech's "Kai" microsurgical robotic system to reconnect blood vessels less than 0.5 millimeters wide during tissue reconstruction after tumor removal [16].

Innovation Approach

The proven benefits of robotic surgery are driving even more innovation, particularly in the realm of digital intelligence. AI-powered systems are becoming a focus, analyzing surgical videos in real time to improve workflows and identify risks. For instance, Caresyntax has implemented its platform in over 4,000 operating rooms, analyzing 2 million procedures annually [13]. Similarly, Activ Surgical’s ActivSight system uses computer vision to visualize tissue perfusion and blood flow, improving situational awareness during operations [13].

As Bohdan Pomahac, Chief of Plastic and Reconstructive Surgery at Yale Medicine, puts it:

"The technology lowers the bar of who can do very complex procedures, so the learning curve is faster."

[14]

Modular designs are also gaining traction. CMR Surgical's CEO, Massimiliano Colella, highlights this trend:

"There are an increasing number of hospitals that basically are telling us that this modularity will really fit into the idea that they have of a robotic program"

[14]

Other systems are focusing on precision and efficiency. Stryker’s Mako uses 3D CT-based preoperative planning with haptic boundaries to guide bone cuts, while Smith+Nephew’s CORI eliminates the need for preoperative CT scans by relying on real-time intraoperative mapping, reducing radiation exposure [11].

Commercialisation Timeline

Surgical robots come with a hefty price tag, ranging from €1.35 million to €2.25 million, plus annual service fees between €90,000 and €270,000 [11][15]. Medtronic’s Hugo and CMR Surgical’s Versius are marketed as more cost-effective modular options, though overall costs depend on usage volume and service agreements [11][15]. Robotic procedures typically add €2,700 to €5,400 to the cost of traditional laparoscopy due to pricey consumables [12].

In January 2026, Johnson & Johnson submitted its Ottava system for FDA approval. This system integrates directly with the operating table and features a compact design [13]. Intuitive Surgical is also expanding its reach, with nine new FDA-approved indications for cardiac surgeries, including valve repairs, as of 2026 [14]. Adoption is extending beyond hospitals to Ambulatory Surgery Centres, where companies like Moon Surgical are introducing compact, mobile robots designed for high-turnover outpatient procedures [11][14].

CES 2026: Robotics, Physical AI, and Automation

3. Humanoid and General-Purpose Robots

Humanoid and general-purpose robots are no longer confined to factories or medical settings. They're moving into everyday spaces, from homes to hospitals.

Technology Maturity

By 2026, humanoid robots began using Vision-Language-Action (VLA) models. These systems allow robots to understand natural language commands and turn them into physical actions [1][3]. Leading the charge are NVIDIA's GR00T N1.6, with 2.2 billion parameters, and Physical Intelligence's pi-0.5, boasting 3 billion parameters. These "robot brains" enable machines to navigate unpredictable environments like kitchens or hospital hallways [1][3].

However, challenges remain. Battery life is a major hurdle - most humanoid robots, like Tesla's Optimus Gen2, can only operate for 90–120 minutes per charge. This falls far short of the 8 to 20 hours needed for industrial shifts [1]. Experts predict that batteries supporting full-day operation won't be widely available until 2035 [1]. Another issue is the gap between lab performance and real-world reliability. Robots achieving 95% accuracy in controlled settings often drop to 60% in real-world environments, where lighting, surfaces, and human behavior are less predictable [1][3].

"Visual images in simulated environments are pretty good, but the real world has nuances that look different." – Ayanna Howard, Dean of Engineering at Ohio State University [3]

Market Impact

By early 2026, the humanoid robot market had grown to 16,000 installed units worldwide. Projections suggest this will skyrocket to 2 million units by 2035 and 300 million by 2050 [1][3]. The market's value is expected to reach between €1.3 trillion and €1.6 trillion by 2050 [3]. This growth is being fueled by falling manufacturing costs, which dropped 40% between 2023 and 2024 [3].

China's AgiBot led global shipments in 2025, delivering 5,100 units and claiming a 39% market share [1][2]. The company's success stems from aggressive mass production at its Shanghai facility, focusing on affordable solutions [1][2]. Meanwhile, Tesla deployed over 1,000 Optimus robots in its factories by January 2026, with plans to scale up to 50,000 units by the end of the year [1].

Geographic trends are becoming clear: China excels in mass production and supply chain efficiency, while the United States leads in cognitive AI and advanced industrial applications [1][4]. As of 2026, 90% of critical robotics components are still sourced from China, creating dependencies for Western manufacturers [1].

Innovation Approach

The robotics industry secured €38.6 billion in funding in 2025, accounting for 9% of all venture capital investment [7]. This funding is driving a shift toward foundation model licensing, where companies license pre-trained AI systems from providers like NVIDIA or Meta instead of building their own from scratch [7]. Companies like World Labs are creating "world models" that help robots predict physical outcomes and adapt to mistakes, enabling them to perform multi-step tasks autonomously [7].

Biomimetic design is also gaining traction. DroidUp's Moya, for example, features "warm skin" and micro-expressions to make interactions with humans more natural [2]. For consumer-focused robots, 1X's NEO uses a "human-in-the-loop" system, where remote operators oversee complex tasks while the AI gradually learns [19].

Commercialisation Timeline

Robot pricing varies widely depending on their capabilities. Tesla's Optimus is targeting a future price range of €19,000 to €28,500 [1][19]. In contrast, Boston Dynamics' Atlas, integrated with Google DeepMind, is entering commercial production in 2026 with an estimated price tag of €133,000 to €142,500 [19]. Meanwhile, Amazon's robotic fleet surpassed 1 million units in June 2026, featuring VLA-powered systems that improved travel efficiency by 10% [1][3].

"We have not actually seen any improvement in widely deployed robotic hands or end effectors in the last 40 years." – Rodney Brooks, robotics pioneer [1]

Despite rapid advancements in AI, hardware limitations - especially in dexterous manipulation - remain a bottleneck. As costs drop and capabilities improve, the robotics industry is poised for further growth, setting the stage for a deeper look into these strengths and challenges in the next section.

4. Warehouse and Logistics Automation

Warehouse and logistics automation has evolved from a niche experiment to a core necessity. By 2026, this sector is projected to be worth between €9.5 billion and €14.2 billion, with an annual growth rate of 15–20% [5]. This rapid expansion mirrors broader advancements in physical AI across industrial, medical, and humanoid applications. At the heart of this shift are Vision-Language-Action (VLA) models, which enable robots to interpret visual inputs and language commands, transforming them into actionable tasks. These models are replacing outdated scripted routines [1,4]. For example, AI-powered orchestration platforms like LocusONE are now capable of managing mixed teams of robots and humans by predicting congestion and dynamically reallocating resources [20].

Technology Maturity

The industry is moving away from traditional Person-to-Goods (P2G) systems - where robots assist humans - to fully autonomous Robots-to-Goods (R2G) workflows. In these setups, robots independently handle tasks like transport, replenishment, and returns [20]. However, challenges remain, such as the "sim-to-real" gap. Robots that perform with 95% accuracy in controlled lab settings may see that drop to 60% in unpredictable real-world environments due to factors like lighting and surface variations [1].

Specialized robots outperform humanoid designs in warehouse settings. For instance, Boston Dynamics' Stretch robot has proven its worth by unloading containers faster than humans and is already being used in GAP warehouses [5]. On the other hand, trials with humanoid robots have highlighted hardware limitations, reaffirming the dominance of purpose-built machines in production environments.

Market Impact

By mid-2026, Amazon's fleet of over 1 million robots is expected to handle 75% of its global deliveries [1]. The demand for collaborative robots is also booming, with shipments projected to exceed 47,000 units by the end of 2026, representing an annual growth rate of more than 37% [21]. One striking example of this trend is Staples Canada, which replaced traditional conveyors with autonomous robots in its largest fulfilment centre near Toronto. This facility now manages nearly 50% of the company’s national e-commerce operations [5].

Exotec, a leader in warehouse robotics, reached €1 billion in cumulative sales by 2024 and has secured over 400 patents. In February 2026, Renault Group deployed 85 of Exotec’s Skypod robots in Germany, processing 107,000 orders daily and improving operational efficiency by 50% [22].

Innovation Approach

Recent advancements in VLA models and the licensing of foundation models have shifted the focus of warehouse automation towards multi-node networks and predictive orchestration. Locus Robotics is leading the charge with its multi-node network approach, which connects smaller fulfilment centres into a unified system. This setup enables virtual labour and capacity sharing, significantly reducing worker walking distance and travel time - by as much as 80% [20].

NVIDIA is also making waves, positioning itself as a key infrastructure provider with its Isaac GR00T foundation models and Jetson T4000 edge compute modules, priced at €1,900 per unit. The company aims to establish itself as the "Android of robotics" [1]. Additionally, the trend toward licensing pre-trained AI systems rather than building them from scratch is gaining momentum, streamlining the adoption process for businesses [7].

"Continuous improvement isn't a department. It's a mindset." – Tony Altman, Motivational Fulfillment [20]

Costs for these innovations vary widely. Boston Dynamics' Stretch robot is priced between €285,000 and €475,000 per unit [5], while Tesla’s Optimus robot is targeting a more accessible price range of €19,000 to €28,500 [1]. However, achieving reliable performance remains a hurdle. For production environments, 99.9% accuracy is essential. A robot operating at 95% accuracy could fail about 50 times per day, requiring frequent human intervention [1]. These advancements underscore the industry's push toward smarter, more integrated AI-driven systems, which are reshaping the future of warehouse automation.

5. AI Infrastructure Providers

Technology Maturity

The infrastructure supporting robotics has advanced significantly, with NVIDIA leading the charge through its comprehensive, full-stack approach. From Jetson robotics processors to tools like CUDA, Omniverse, and open physical AI models such as Cosmos and GR00T, NVIDIA has built a robust ecosystem [23]. Its Jetson T4000 stands out, delivering 1,200 FP4 TFLOPS while being four times more energy-efficient than earlier models. This is achieved within a 70-watt power envelope, with units priced around €1,900 for orders of 1,000 or more [23]. This level of edge computing ensures robots can make critical safety decisions on-site, without depending on cloud connectivity [18]. Such advancements are directly tied to the improvements in real-world robot performance discussed earlier.

Microsoft has also entered the robotics space with Rho-alpha (ρα), an evolution of its Phi series. This model enhances vision-language-action capabilities by incorporating tactile sensing and feedback from human interactions [9]. Meanwhile, Hugging Face has established itself as a hub for open-source robotics, integrating NVIDIA's Isaac and GR00T technologies into its LeRobot framework, which now supports 13 million AI developers [1][23]. On the data front, Meta has invested €14 billion in Scale AI, securing infrastructure for data and model development [7].

Market Impact

These technological leaps are reshaping the robotics industry. In 2025, robotics funding hit a record €38.6 billion, accounting for 9% of all venture capital investments [7]. Funding for "world models", which enable robots to predict spatial relationships and physical interactions, soared from €1.3 billion in 2024 to €6.5 billion in 2025 [7]. This marks a shift from rigid programming to adaptable, task-specific systems, accelerating adoption across various sectors. For instance, in January 2026, LEM Surgical used NVIDIA Isaac and Cosmos Transfer to train the autonomous arms of its Dynamis surgical robot, leveraging the NVIDIA Jetson AGX Thor [23]. Around the same time, Caterpillar expanded its partnership with NVIDIA to incorporate advanced AI and autonomy into construction and mining equipment [23].

"The ChatGPT moment for robotics is here. Breakthroughs in physical AI - models that understand the real world, reason and plan actions - are unlocking entirely new applications." - Jensen Huang, Founder and CEO, NVIDIA [23]

Innovation Approach

AI infrastructure providers are focusing on creating integrated ecosystems that blend proprietary tools with open-source resources, connecting millions of developers through unified platforms [1][23]. These efforts are crucial for advancing the industrial, medical, and humanoid systems discussed earlier. In January 2026, NVIDIA launched its OSMO orchestration framework, which was immediately integrated into the Microsoft Azure Robotics Accelerator toolchain. This framework simplifies workflows by combining synthetic data generation, model training, and simulation testing into a single platform [23].

Synthetic data is playing a key role in overcoming the challenge of limited real-world data. With tools like NVIDIA Isaac Sim on Azure, developers can now generate accurate, physics-based data in just 36 hours - compared to the months it would take to collect manually [1][9]. However, the "sim-to-real" gap remains a hurdle; policies that perform well in simulation (95% success rates) often drop to 60% in real-world conditions due to differences in lighting and textures [1]. To address this, platforms like Foxglove and Formant are stepping in, offering real-time monitoring of deployed robots and feeding edge-case data back into training systems [7].

6. New Startups to Watch

Technology Maturity

Startups are reshaping robotics by shifting from rigid programming to more adaptable, AI-driven platforms. A standout in this field is Physical Intelligence, which champions the "Universal Robot Brain" concept. Their foundation model, pi‑0.5, allows robots to learn tasks like folding laundry or assembling electronics without needing specific programming for each task. This model has been trained across seven platforms, 68 tasks, and 104 homes - marking a departure from traditional hard-coded approaches [1]. Similarly, Skild AI has developed its Skild Brain, leveraging massive datasets of video and robot interactions to create a general-purpose intelligence that works across diverse platforms, including quadrupeds, bipeds, and robotic arms [24].

1X Technologies, with backing from OpenAI, takes a different approach by focusing on soft robotics. Their NEO robot uses muscle-like actuators, prioritizing safety in home environments rather than the high-torque designs common in industrial robots [25]. Sunday Robotics is targeting households with a dual-armed wheeled robot trained on 10 million household scenarios. They utilize a proprietary Skill Capture Glove to gather high-quality human demonstration data [24]. Meanwhile, in China, AgiBot (Zhiyuan) is making waves with its "China Speed" strategy, emphasizing rapid mass production and affordability to dominate the global mid-market for industrial humanoids. By 2025, they shipped 5,100 units, capturing around 39% of the global market share [1][2].

These advancements highlight the technical progress setting the stage for broader market shifts.

Market Impact

The robotics sector is attracting significant investment, with startups raising over €5.7 billion in the first seven months of 2025 alone. This trend shows a focus on channeling funds into fewer but larger frontier companies [1]. Physical Intelligence secured €570 million in Series B funding, achieving a valuation of €5.3 billion. Skild AI raised €1.3 billion and quickly generated €28.5 million in revenue through deployments in security, warehousing, and manufacturing [1][26]. Figure AI, another key player, reached an impressive €37 billion valuation after a €950 million Series C round in September 2025 [1].

"Think of it like ChatGPT, but for robots." - Sergey Levine, Co-founder, Physical Intelligence [26]

The global embodied AI market hit €4.2 billion in 2025, growing at an annual rate of 39%. However, startups face a significant challenge: a reliability gap. While lab-tested policies often achieve 95% success rates, real-world deployments see a drop to 60% due to environmental factors like lighting and textures [1]. To tackle this, Standard Bots offers AI-native robotic arms that learn tasks through demonstration. Operators can guide the arm manually, simplifying integration for small and medium-sized enterprises (SMEs) [25].

Commercialization Timeline

The most promising startups are aiming for broader industrial pilots between 2026 and 2028, with commercial deployments anticipated from 2028 to 2032 [2]. In February 2026, Apptronik raised €494 million in a Series A extension to scale production of its Apollo humanoid robot, designed for logistics and manufacturing [27]. Around the same time, Weave Robotics began shipping Isaac 0, the first residential robot specifically designed for autonomous laundry folding [27]. Sunday Robotics plans to move from stealth mode to beta testing by late 2026, aiming to price its home assistant robot below €9,500 [24].

While these developments are promising, challenges remain. Battery limitations continue to hinder progress, and actuators still account for 60% to 70% of manufacturing costs. However, production expenses for humanoid robots dropped by 40% between 2023 and 2024 [1][3]. By 2035, material costs are expected to fall to between €12,350 and €16,150 per unit, potentially enabling mass adoption and the deployment of an estimated 2 million humanoids in workplaces [3].

Strengths and Weaknesses

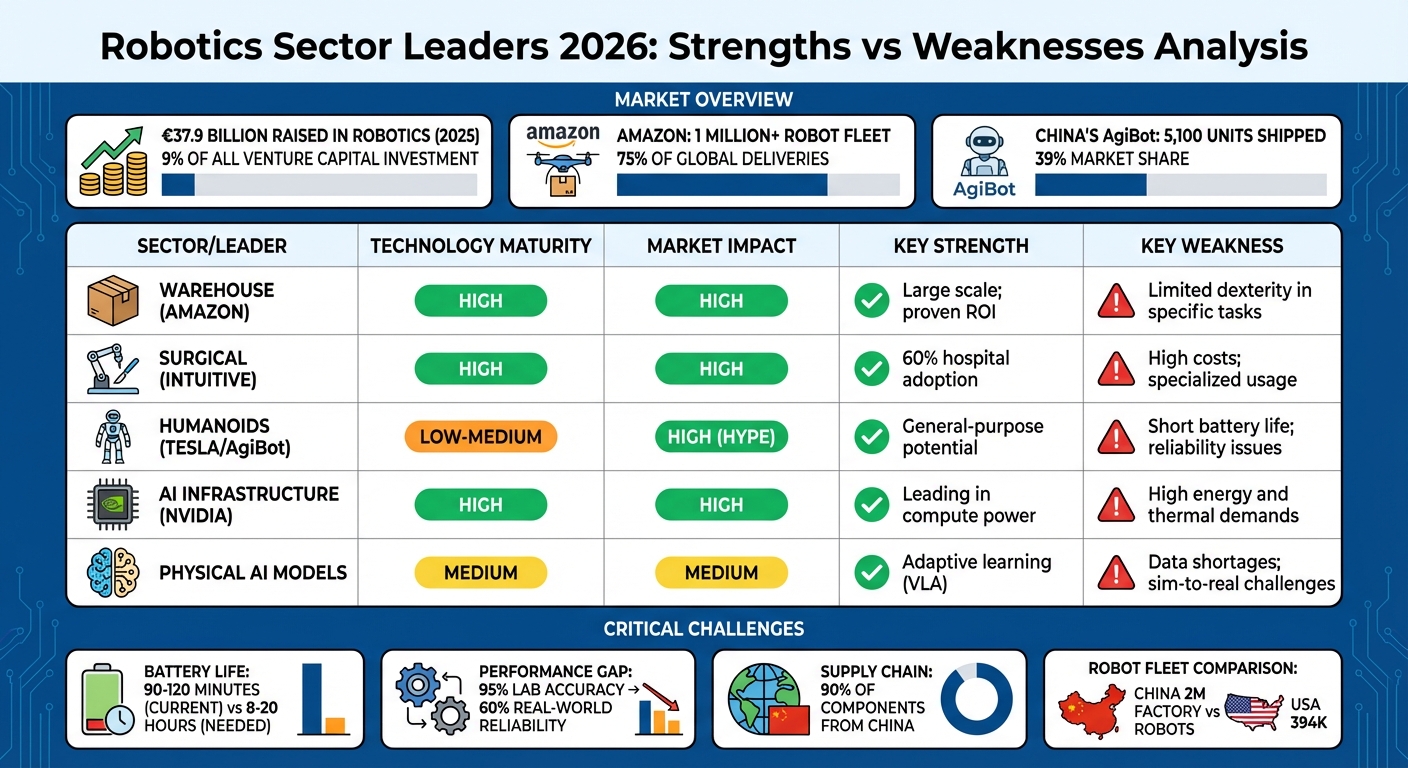

Robotics Sector Leaders 2026: Market Impact and Technology Maturity Comparison

This section brings together the main advantages and challenges discussed earlier, showing the trade-offs across different robotics sectors. By 2026, the robotics landscape paints a clear picture: well-established areas like warehousing and surgical robotics are delivering consistent results, while newer humanoid platforms still struggle with fundamental issues. For example, Amazon’s warehouse fleet crossed the 1 million mark in June 2026, with its DeepFleet AI boosting travel efficiency by 10% across its network [1]. Similarly, surgical robotics have reached 60% adoption in large hospitals, with robotic-assisted procedures now accounting for 55% of complex surgeries in developed nations [1].

However, real-world performance often lags behind lab results. Despite achieving 95% accuracy in controlled environments, performance can drop to 60% in actual conditions due to environmental factors [1]. Robotics pioneer Rodney Brooks highlighted this gap:

"We have not actually seen any improvement in widely deployed robotic hands or end effectors in the last 40 years... deployable dexterity will remain 'pathetic compared to human hands' beyond 2036" [1].

Humanoid robots face additional hurdles, such as limited battery life - lasting only 90 to 120 minutes, far below the 8 to 20 hours required for industrial use [1]. Solid-state batteries offer potential, but they likely won’t scale for robotics until 2035 [1]. Manufacturing costs have improved, with a 40% reduction between 2023 and 2024, yet actuators remain costly, making up 60–70% of total production expenses [1][3].

The table below summarizes the strengths and weaknesses across key sectors:

| Sector / Leader | Technology Maturity | Market Impact | Key Strength | Key Weakness |

|---|---|---|---|---|

| Warehouse (Amazon) | High | High | Large scale; proven ROI | Limited dexterity in specific tasks |

| Surgical (Intuitive) | High | High | 60% hospital adoption | High costs; specialized usage |

| Humanoids (Tesla/AgiBot) | Low-Medium | High (Hype) | General-purpose potential | Short battery life; reliability issues |

| AI Infrastructure (NVIDIA) | High | High | Leading in compute power | High energy and thermal demands |

| Physical AI Models | Medium | Medium | Adaptive learning (VLA) | Data shortages; sim-to-real challenges |

Regional differences also play a big role in shaping these strengths and weaknesses. U.S. companies focus on vertical integration and reliability, with firms like OpenAI and NVIDIA driving advancements in cognitive AI [4][8]. Meanwhile, Chinese manufacturers, such as AgiBot, emphasize rapid production and cost efficiency. AgiBot shipped 5,100 units in 2025, securing 39% of the global market [1]. Currently, China operates 2 million factory robots, dwarfing the U.S. figure of 394,000. Additionally, about 90% of key robotics components are still sourced from China as of 2026 [1]. This heavy reliance on Chinese supply chains poses geopolitical risks, especially as the U.S. plans to ban Chinese autonomous vehicle software by 2027 and hardware by 2030 [1].

Conclusion

By 2026, NVIDIA stands at the forefront of robotics, with its Isaac GR00T and Cosmos models driving advancements across multiple manufacturers. Meanwhile, Amazon operates an impressive fleet of over 1 million robots, handling 75% of global deliveries, and China's AgiBot has carved out a strong position in the humanoid market, shipping 5,100 units and capturing 39% of the market share [1][2].

The robotics industry hit a record €38.5 billion in venture funding in 2025, accounting for 9% of all venture capital. This milestone reflects the sector's evolution from experimental prototypes to large-scale industrial applications [7]. However, scaling up comes with its own set of challenges.

Key obstacles remain. Battery life limits humanoid robots to just 90–120 minutes of operation, far short of the 8–20 hours required for many tasks. Additionally, the "sim-to-real" gap - where robots perform with 95% accuracy in labs but drop to 60% in real-world conditions - highlights the difficulty of transitioning from controlled environments to practical deployment [1].

Despite these hurdles, the industry is already pushing boundaries. Multi-robot coordination and Vision-Language-Action models, which enable robots to learn from video demonstrations, are emerging as the next big goals. Investment in advanced world models surged from €1.3 billion in 2024 to €6.5 billion in 2025, with companies like Physical Intelligence and Skild AI leading the charge [7].

Looking ahead, the industry's growth will depend on overcoming reliability issues, diversifying supply chains (currently, 90% of components come from China), and adopting scalable solutions like Robotics-as-a-Service [1]. The organizations that can balance bold innovation with practical deployment will shape the path of robotics through 2030 and beyond.

FAQs

What is “Physical AI” in robotics?

Physical AI in robotics is all about creating systems that allow machines to perceive, think, and interact with their surroundings in real time, all while operating with a high level of independence. Unlike traditional robots that follow pre-programmed instructions, these systems are designed to learn and adapt on the go.

By combining advanced sensors like cameras and radar with data-driven models, these robots can handle complex tasks in dynamic environments. This means they’re not just performing repetitive actions - they’re making decisions and solving problems in real-world scenarios. Whether it’s assisting in delicate surgeries, navigating busy city streets, or inspecting industrial sites, these intelligent agents are built to thrive in unpredictable situations.

Why do robots drop from lab accuracy to real-world reliability?

Robots frequently face a decline in performance when moving from the controlled precision of lab settings to the unpredictable demands of real-world environments. While labs offer stable and consistent conditions, they can't fully mimic the complexity of real-life scenarios. Out in the field, robots must contend with unexpected obstacles, sudden changes, and a wide range of situations that are hard to predict during testing. This gap between testing and deployment highlights the challenges of ensuring consistent reliability in diverse, ever-changing environments.

What must improve for humanoid robots to work full shifts?

For humanoid robots to handle full work shifts, several areas need attention. First, battery technology must advance to provide longer operational periods and cut down on recharging breaks. Next, enhancing hardware durability is key to reducing frequent maintenance or repairs. Finally, better AI systems are necessary to tackle unexpected situations, navigate unpredictable settings, and improve autonomy, ensuring robots can operate efficiently for extended periods.